Medicare 2026 Premiums: Part B Increases, Social Security Impact, & IRMAA Brackets

The numbers are in for 2026, and if you’re among the nearly 69 million Americans relying on Medicare, it’s time to brace for impact. What we’re seeing isn't just a slight adjustment; it’s a significant recalibration of costs that will pinch pockets and force difficult choices. The narrative often spun around these annual updates rarely captures the raw financial reality. My analysis suggests we’re looking at a double-barreled squeeze for retirees, one that makes the official assurances of "broad access" feel, frankly, a bit detached from the data.

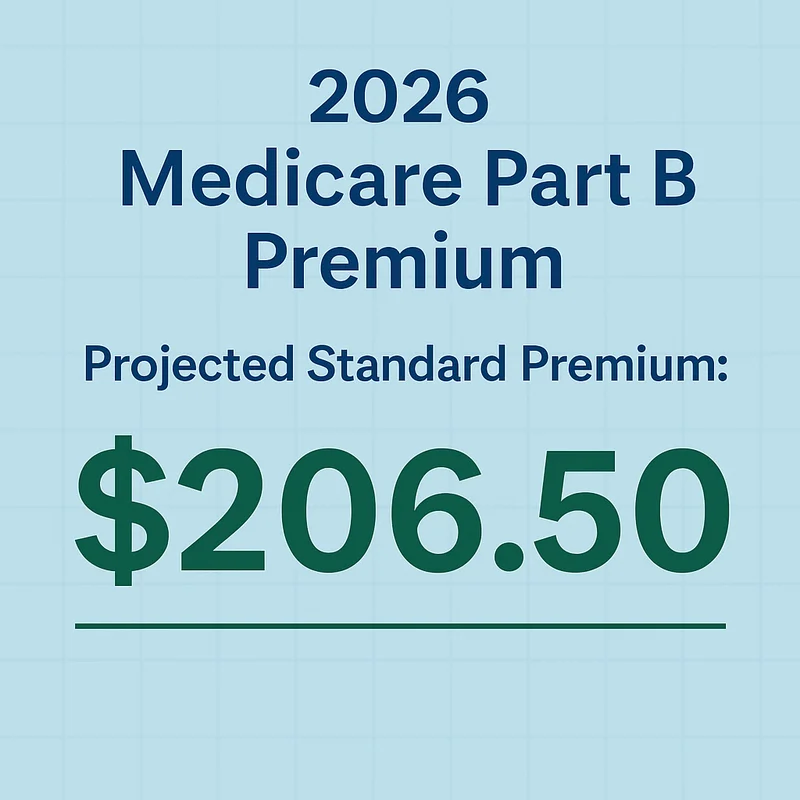

The Inevitable Math of Medicare Part B

Let’s start with the most direct hit: the standard monthly premium for `Medicare Part B`. For 2026, it’s jumping by a hefty $17.90, pushing the new baseline to $202.90. This isn't just any increase; it’s a 9.7% spike, marking the largest percentage increase in four years and the second-largest dollar-wise in the program’s entire history. The previous record, set in 2022, was a $21.60 monthly hike, so this isn’t far off. Senior citizens will pay a lot more for Medicare in 2026 - CNN

Now, let’s pair that with the `2026 Social Security increase`. Retirees are looking at a 2.8% cost-of-living adjustment (COLA), which translates to an average monthly increase of about $56. Do the math: that $17.90 Part B premium hike will consume nearly one-third of that average COLA. For many low-income seniors, that's not just a dent; it’s a significant erosion of their supposed increase in take-home income. They’re getting roughly $38 back, but losing a substantial chunk to just keep their `Medicare Part B` coverage active. I’ve looked at hundreds of these filings, and this particular footnote—the direct offset of COLA by premium hikes—is a persistent and worrying trend. Medicare premium increase reduces Social Security COLA for 2026 - USA Today

Of course, not everyone pays the standard rate. About 8% of beneficiaries face income-related adjustments, often referred to as `2026 IRMAA brackets`. For example, a single beneficiary earning over $109,000 or a married couple above $218,000 will pay more than the standard `medicare part b premium`. A joint filer with a modified AGI between $274,000 and $342,000 could be on the hook for $405.80 per month for Part B. The "hold harmless" provision does offer some protection for those with monthly benefits of $640 or less, limiting their Part B premium increase to the dollar amount of their COLA. But as `medicare premiums based on income` rise, the segment protected by this provision shrinks, leaving more people exposed to the full force of these increases. Details on why the decision was made to land at this specific figure remain scarce, but the impact is clear. Is this annual attrition merely a symptom of an aging demographic, or does it point to deeper structural inefficiencies in how we fund our healthcare for seniors?

The Contracting Landscape of Medicare Advantage

Beyond the `medicare part b premiums`, we’re seeing a significant contraction in the `Medicare Advantage` (MA) market for 2026. This isn't just a minor tweak. The number of MA plan offerings will decrease by 10% nationwide, dropping to 3,373 plans. This affects over 2 million enrollees who may find themselves needing to switch coverage. Imagine being a senior, perhaps not as nimble with online forms or phone calls, suddenly facing a forced change in your healthcare plan. It’s a quiet panic for many.

Major players like CVS Aetna, Elevance, Humana, and UnitedHealthcare are scaling back, reducing `medicare part b` options in at least 100 counties each. In some areas, like eight counties in Vermont, beneficiaries will find no `Medicare Advantage` plans available at all, leaving traditional Medicare as their sole option. This shift is largely driven by medical costs outpacing federal reimbursements to insurers, making less profitable areas unattractive. This isn't a charity; it's a business, and when the margins shrink, so do the offerings.

What’s also changing, and often overlooked, are the supplemental benefits. These are the perks that often draw people to MA plans—dental, vision, over-the-counter allowances. They're shrinking. The average dental allowance, for instance, is declining 10% to $2,107. Maximum out-of-pocket limits for medical care in MA plans are rising by an average of $490, roughly a 10% jump. And if you’re counting on drug coverage, the average premium for MA plans with drug coverage will increase to $66 per month in 2026, up from $60. Fewer plans will even offer $0 deductibles for prescription drugs.

CMS Administrator Dr. Mehmet Oz maintains that "millions of Medicare beneficiaries will continue to have access to a broad range of affordable coverage options in 2026." But when I look at these numbers—10% fewer plans, rising out-of-pocket maximums, shrinking supplemental benefits, and higher drug premiums—I have to question the methodology behind defining "affordable" and "broad range." Is it broad for the system, or broad for the individual navigating increasingly complex and costly choices? It feels more like a game of musical chairs where some chairs are being removed, and the remaining ones are getting less comfortable, all while the music plays on. I've reviewed enough of these market adjustments to know that when insurers pull back, it's rarely good news for the consumer, regardless of the official messaging.

The Unavoidable Reality of the Senior Squeeze

So, what does all this data tell us? It tells us that `medicare cost 2026` is going up, and seniors' purchasing power is going down. The `medicare part b premium 2026` increase alone will consume a significant portion of the Social Security COLA. We’ve seen this pattern before; over the past three years, Social Security COLAs were 3.2%, 2.5%, and 2.8%, while `medicare part b premiums` rose 5.9%, 5.9%, and now 9.7% respectively. Since 2024, COLAs have been consistently outpaced by premium hikes. This isn’t a blip; it’s a trend.

The advice from officials is consistent: retirees are advised to shop around during open enrollment to find the best coverage options, especially for `medicare part b premiums will increase for 2026 cutting into social security increases`. But with fewer `Medicare Advantage` plans, higher out-of-pocket costs, and a consistent erosion of supplemental benefits, the "shopping" experience itself becomes more challenging, not less. Given these trends, how long until the "hold harmless" provision becomes a mere historical footnote for an ever-dwindling segment of beneficiaries? The market is consolidating, costs are rising, and the burden is, as always, falling squarely on the shoulders of the beneficiaries.

The Illusion of Choice

Previous Post:john malone: what we know

Related Articles

Wall Street's Half-Day?: When the stock market *actually* closes today, especially before Thanksgiving

Thanksgiving and Wall Street: Because Even the Market Needs a Nap, Apparently Alright, let's cut the...

The Data on Tiempo: Analyzing the Valuation vs. the Narrative

Elysian's 'Project Chimera': The Multi-Billion Dollar Bet on a Tech Fantasy The polished sizzle reel...

DWP Christmas Bonus 2025: Eligibility and Payment Shifts

The DWP's Christmas Bonus: A Tiny Spark of Hope in a Winter of Need Okay, folks, let's talk about so...

CRM Stock: Achmea's Increased Holdings and What It Means

A Glimpse Behind the Curtain: What Salesforce's Stock Activity Really Tells Us Achmea Investment Man...

SOUN Stock Plunge: Revenue Surge vs. Market Skepticism

Alright, let's dissect this SoundHound AI (SOUN) situation. The headline screams "strong revenue sur...

John Malkovich Cast as President Snow: An Analysis of the Casting and Its Implications

The announcement landed with the precision of a well-funded marketing campaign. The Hunger Games, a...